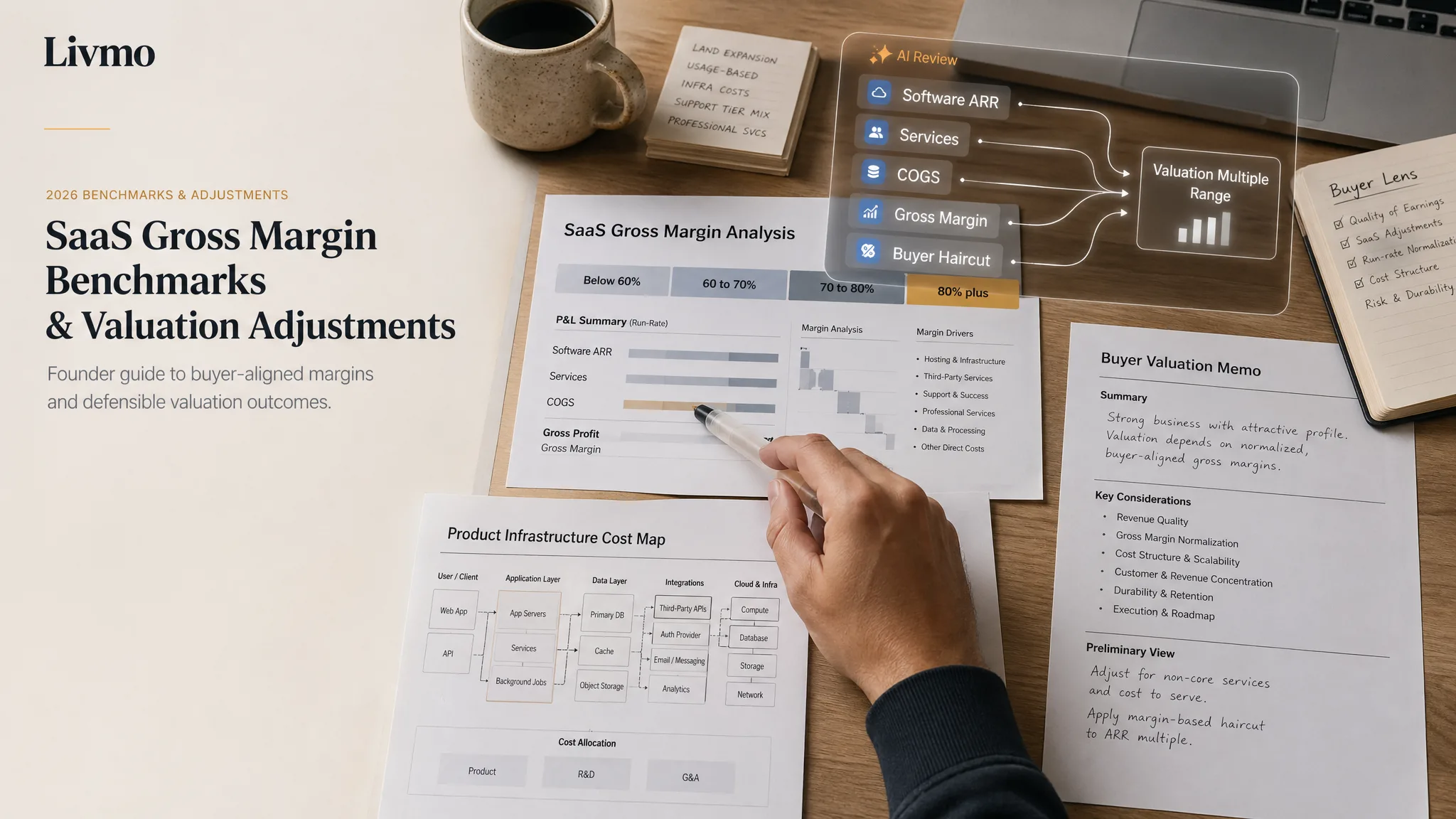

SaaS gross margin benchmarks valuation 2026 comes down to one buyer question: how much of each dollar of ARR turns into recurring software profit? In current benchmarks, 75% software gross margin is the practical floor for a clean SaaS story, while best in class software companies often clear 85%.

Founders usually optimize growth, retention, and EBITDA first. Gross margin sits quietly in the model until diligence starts. Then buyers separate software ARR from services revenue, reclassify support and hosting costs into COGS, and price the business on the margin profile they believe is repeatable.

Why SaaS gross margin benchmarks valuation 2026 matters

A high margin says the product scales. A low margin says the buyer may be buying labor dressed up as software.

G Squared Partners’ 2026 SaaS benchmark guide says software subscriptions should aim for 75% or higher gross margin. Axial’s 2026 SaaS multiples guide puts the target above 75%, with best in class companies above 85%.

That range matters because buyers do not pay the same multiple for every dollar of revenue. A dollar of self serve subscription ARR with low delivery cost is worth more than a dollar that requires implementation work, managed services, heavy support, or expensive compute.

The 2026 software gross margin benchmark most buyers expect before they treat revenue as clean, scalable SaaS ARR.

This is why gross margin belongs beside retention in the valuation conversation. I wrote separately about how net revenue retention changes SaaS valuation. Gross margin answers the companion question: how profitable is that retained revenue after delivery costs?

The four gross margin bands buyers use

Here is the simple way I frame it with founders. The exact multiple depends on growth, retention, market, size, and buyer fit. But gross margin changes the buyer’s confidence in the revenue base.

| Gross margin band | Buyer read | Likely valuation effect |

|---|---|---|

| Below 60% | Services heavy, support heavy, or compute heavy | ARR gets questioned. Some revenue may be valued closer to services revenue. |

| 60% to 70% | Functional, but not premium SaaS | Multiple pressure unless growth and retention are strong. |

| 70% to 80% | Acceptable SaaS profile | Usually defensible if COGS are clean and services are separated. |

| Above 80% | Scalable software economics | Supports premium positioning when paired with strong retention and growth. |

Below 60%, the buyer asks whether the business is really SaaS. This is where implementation revenue, customer specific configuration, outsourced support, and infrastructure costs start to dominate the discussion.

From 60% to 70%, the buyer may still like the company, but the multiple usually has a ceiling. The story becomes less about pure software scalability and more about operational cleanup.

From 70% to 80%, you are in the normal zone. You still need clean cost classification. You also need to show that onboarding, support, hosting, and customer success costs do not rise linearly with revenue.

Above 80%, gross margin becomes a positive signal. The buyer can believe that incremental ARR drops through the model. If retention is strong, this is where valuation starts to get more interesting.

Gross margin does not create a premium by itself. It protects the premium that growth, retention, and market quality already earned.

How the bands change offers at $2M, $5M, and $10M ARR

The math gets louder as ARR grows because each margin point affects more future cash flow.

At $2M ARR, a buyer may tolerate lower margin if the product is early, the team is lean, and the customer base is sticky. But if gross margin is below 60%, buyers will usually haircut the ARR base before applying a multiple. They may treat services revenue separately or normalize COGS upward.

At $5M ARR, the excuses fade. Buyers expect a real finance function, cleaner COGS, and evidence that support and hosting costs are not quietly scaling with every customer. This is also where a quality of earnings process will test the numbers. If you have not prepared for that, read my guide to what a quality of earnings report actually tests.

At $10M ARR, gross margin becomes a board level issue for the buyer. A company doing $10M of ARR at 82% gross margin has a very different future cash flow profile than one at 62%. Even if both show the same ARR, the buyer is underwriting different operating models.

Benchmarkit and G Squared cite compressed median net revenue retention around 101%, which means buyers are paying closer attention to margin and efficiency when growth is harder to buy.

SaaS Capital’s 2026 bootstrapped SaaS benchmarks found median revenue growth of 15%, median NRR of 103%, and median GRR of 91% for bootstrapped companies with $3M to $20M in ARR. When growth is measured and retention is only modestly above 100%, cleaner margin can carry more weight in the buyer’s model.

The founder mistake is assuming ARR size controls the conversation. It does not. ARR size gets you into the buyer’s filter. Gross margin helps decide how much of that ARR the buyer trusts.

Why services revenue gets a different haircut

Services revenue is not bad. Implementation, migration, training, and managed services can help customers succeed. The problem starts when services are blended into ARR and presented as if they have the same economics as subscription revenue.

Buyers separate the streams. Subscription revenue with 80% gross margin might support a software multiple. Services revenue with 30% to 50% gross margin usually will not. If the service work is required to deliver the product, the buyer may also question whether the software is truly repeatable.

This is the silent multiple killer in founder led SaaS companies. The P and L says revenue is growing. The diligence file says some of that growth needs human delivery. Those are not the same thing.

If services are strategic, show them separately. Break out software subscription revenue, implementation revenue, support costs, hosting costs, and services labor. Clean separation gives buyers less room to apply a broad discount.

The same logic shows up in add backs. Buyers accept clean, well supported adjustments and reject messy ones. I covered that pattern in EBITDA add backs buyers actually accept. Gross margin adjustments work the same way. Evidence wins. Vague explanations lose.

What to fix before buyers see the model

First, rebuild COGS the way a buyer will. Include hosting, third party software required to deliver the product, customer support tied to delivery, implementation labor, and any customer success work that is really service delivery.

Second, split subscription and services revenue. Do not make buyers do it for you. If the business has services attached to onboarding, show attach rate, gross margin, and whether services shrink as customers mature.

Third, show margin trend by cohort or customer segment if possible. Enterprise customers may carry lower support costs after onboarding. SMB customers may look higher margin but churn faster. The cleanest story is not always the highest average. It is the story buyers can verify.

Fourth, explain AI or compute costs clearly. High Alpha’s 2025 SaaS benchmarks note that AI is now core across new software companies. G Squared also points out that AI native companies can carry lower gross margins because inference and compute costs are real. If AI costs are in your model, buyers need to see pricing power, usage controls, and margin improvement over time.

Do not wait for diligence to discover your real gross margin. Recast it before market, then decide whether to fix pricing, COGS, or services packaging.

How to Prove Your Gross Margin Is Buyer Ready

The percentage matters, but the accounting behind it matters more.

A buyer will test whether your SaaS gross margin benchmark uses a consistent definition. Hosting, third party data, implementation labor, customer support, and payment processing can move between COGS and operating expenses. Moving a cost below gross profit does not improve the economics.

Build a monthly bridge from reported gross profit to normalized software gross profit. Separate subscription revenue from services and show the direct delivery costs for each stream. If infrastructure costs changed after a migration or pricing change, document the timing and the recurring run rate.

A defensible 75% gross margin is worth more than an 85% figure a buyer cannot reproduce from the ledger.

For 2026 comparisons, show both the current margin and the trailing twelve month trend. Buyers want to know whether scale is improving unit economics or whether support and infrastructure costs rise with every new dollar of ARR. Reconcile the schedule to the same records used in a quality of earnings review before the sale process begins.

Frequently Asked Questions

What is a good gross margin for SaaS?

A good SaaS gross margin is usually 75% or higher for software subscriptions. Best in class software companies often exceed 85%, especially when hosting, support, and delivery costs are controlled.

Does gross margin affect SaaS valuation?

Yes. Gross margin affects how much of ARR a buyer views as scalable software revenue. Low gross margin can reduce the multiple or cause buyers to value services revenue separately.

What gross margin do buyers expect?

Most buyers expect software gross margin above 75% before they treat revenue as clean SaaS ARR. Below 70%, they usually dig harder into COGS, services, support, and infrastructure cost allocation.

How do buyers adjust valuation for low gross margins?

Buyers may haircut ARR, apply a lower revenue multiple, separate services revenue, or normalize COGS upward. The adjustment depends on whether the lower margin is temporary, fixable, or structural.

Next Steps

If your SaaS margin story is not buyer ready yet, fix it before the process starts. I can help you see how buyers will recast revenue, COGS, and services before they price the company.