A SaaS financial model in M&A due diligence is not just a forecast. It is a trust test. Buyers compare the model against cohort retention, CAC payback, contraction MRR, hiring capacity, and the ARR bridge before they believe the offer math.

That matters more in 2026 because buyers are still selective. SaaS Capital’s 2026 survey of more than 1,000 private B2B SaaS companies shows bootstrapped companies with $3M to $20M ARR at 15% median growth, 103% median NRR, and 91% median GRR. A seller model that ignores those realities does not make the business look ambitious. It makes the process look sloppy.

What Buyer Expectations Mean for a SaaS Financial Model

A good model does not impress buyers. It removes reasons to doubt you.

Most founders think buyers want a clean revenue forecast, expense forecast, and EBITDA line. They do. But that is only the surface. In a real process, buyers use the model to answer a different question: does management understand the mechanics of the business well enough to own its numbers?

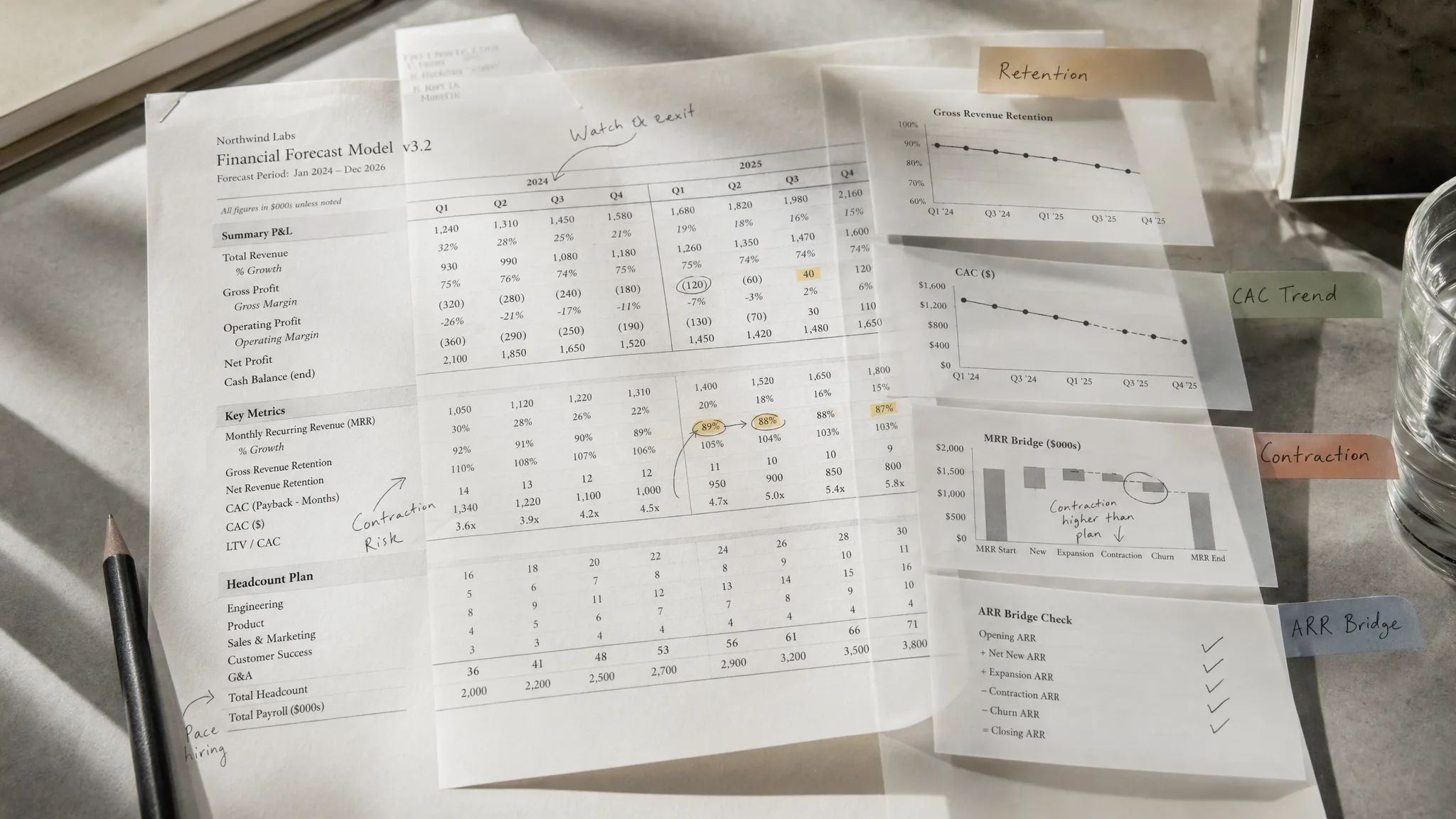

That is why a buyer will trace assumptions back to source data. They will compare the forecast to your customer cube, CRM, billing system, churn history, product roadmap, and hiring plan. If those sources tell different stories, the buyer starts cutting credibility before they cut valuation.

SaaS Capital’s 2026 benchmark for bootstrapped SaaS companies with $3M to $20M ARR gives buyers a realistic baseline for expansion and contraction assumptions.

This is also why your model should match the same underlying numbers you use in your M&A data room preparation checklist. If the model says one thing and the data room says another, the buyer will trust neither.

The Five Signals Buyers Read in Your Financial Model

When I review a seller model, I care less about whether the spreadsheet looks polished and more about whether the assumptions are earned. Buyers think the same way. Five signals matter most.

| Model signal | What buyers check | Why it matters |

|---|---|---|

| Cohort churn | Logo churn, GRR, NRR by customer cohort | Shows whether revenue durability is real |

| CAC assumptions | Actual funnel conversion, spend, payback period | Tests whether growth can be repeated |

| Contraction MRR | Downgrades, seat reductions, usage declines | Reveals hidden weakness inside retained logos |

| Hiring plan | Quota capacity, support load, product roadmap | Shows whether the forecast can be executed |

| ARR bridge | Beginning ARR, new, expansion, contraction, churn, ending ARR | Proves the revenue story reconciles |

Cohort churn is first because it tells buyers whether the forecast is built on a stable base. ChartMogul’s retention report found SaaS companies with NRR above 100% grew 43.6% annually, compared with 13.1% for companies below 60% NRR. That is why buyers do not accept a single blended churn rate when the cohort data says otherwise.

CAC is second because growth claims are cheap. A model that assumes new bookings acceleration needs proof from pipeline conversion, sales cycle length, and payback. G Squared’s 2026 SaaS benchmark work cites median CAC payback around 18 months, with larger ACV segments often stretching to 22 to 24 months. If your model assumes a sudden payback improvement, explain what changes.

Contraction MRR is third because it is where weak models hide churn. A company can show healthy logo retention while existing customers quietly reduce seats, modules, or usage. Buyers will separate expansion from contraction because netting them together can make the base look cleaner than it is.

The strongest seller models let buyers trace every major assumption back to operating evidence. Weak models ask buyers to trust management without proof.

SaaS Financial Model M&A Due Diligence Starts With the ARR Bridge

If the ARR bridge does not reconcile, nothing downstream matters.

The ARR bridge is the spine of a SaaS model. It should show beginning ARR, new ARR, expansion ARR, contraction ARR, churned ARR, reactivation if relevant, and ending ARR. Each line should tie to customer level data.

Buyers know that ARR definitions vary. They will ask whether ARR includes usage revenue, one time fees, paused accounts, discounts, services, and signed but not live contracts. This is the same diligence instinct behind a quality of earnings review: normalize the number before pricing the business.

A clean ARR bridge also protects you during negotiation. If a buyer finds unexplained gaps after LOI, they can use them to reopen price, add an earnout, widen the escrow, or slow the process. If you find and explain them first, the same issue becomes context instead of surprise.

Do not bury adjustments in a hidden tab. Put the definitions, exclusions, and reconciliation logic where a buyer can see them. Confidence comes from transparency.

The Forecast Must Match the Operating Plan

A model can be mathematically correct and still fail diligence. The common reason is that the forecast assumes a company that does not exist yet.

If new ARR doubles, buyers will ask which reps produce it, when they start, how long they ramp, what quota they carry, and whether the pipeline supports it. If gross margin improves, they will ask what hosting, support, and implementation costs change. If retention improves, they will ask which customer success motion creates the change.

That is where founder optimism gets expensive. A buyer does not need you to forecast conservatively. They need you to forecast credibly. Querio’s 2026 M&A preparation guide notes that due diligence often runs 30 to 60 days after LOI and that buyers focus on clean financials, customer cubes, retention metrics, contract terms, and credible forecasts. Those are not separate workstreams. They all meet inside the model.

That common post LOI diligence window is short. A model that needs a rebuild after signing can slow momentum when the seller has the least room for error.

How to Prepare the Model Before Going to Market

Start with the buyer’s path, not your spreadsheet tabs. The model should help the buyer move from question to evidence with as little friction as possible.

First, create a customer level ARR schedule that ties to billing and accounting. Second, build cohort retention views that show logo churn, GRR, NRR, expansion, and contraction. Third, document every forecast assumption in plain English. Fourth, connect hiring, product, and support plans to revenue and margin. Fifth, reconcile the model to historical financial statements before anyone else does.

This is exit readiness work, not cosmetic cleanup. It fits with the same preparation we cover in the SaaS exit readiness checklist. The goal is not to build the most complex model. The goal is to build a model buyers can underwrite.

A buyer ready model has three layers: historical truth, operating logic, and forecast discipline. If one layer is weak, valuation confidence drops.

Frequently Asked Questions

Do I need a financial model to sell my SaaS company?

Yes. A serious SaaS buyer expects a model that connects historical performance, ARR movement, retention, CAC, hiring, and forecast assumptions. The model does not need hundreds of tabs, but it does need to reconcile to source data.

What financial information do buyers request in M&A?

Buyers usually request monthly financial statements, ARR and MRR bridges, customer level revenue, churn and retention data, deferred revenue schedules, pipeline data, and forecast support. For SaaS, the customer cube and ARR bridge often get as much scrutiny as the P&L.

How detailed should a seller financial model be?

A seller model should be detailed enough for a buyer to test the major assumptions without guessing. In practice, that means monthly history, customer level ARR movement, clear churn and expansion logic, hiring assumptions, and a forecast that ties back to the operating plan.

What does a buyer look for in a financial model?

A buyer looks for consistency, reconciliation, and believable assumptions. The fastest way to build trust is to show how revenue, retention, CAC, contraction, hiring, and margin assumptions connect to actual company data.

Next Steps

If your SaaS model would raise buyer questions today, fix it before the process starts. We can review the numbers, identify the gaps, and help you understand what buyers will trust.